When you move out and wait to see how much of your security deposit comes back, you're really waiting on one question: what is the landlord allowed to keep? And the honest answer surprises most tenants, because the list of what a landlord can lawfully deduct is much shorter, and much narrower, than the list of things landlords actually try to charge for. In New York, a landlord can only use your deposit for unpaid rent and for real damage beyond normal wear and tear. That's essentially it. They can't treat the deposit as a non-refundable fee, they can't charge more than one month's rent in total, they can't keep money for the ordinary aging and use of an apartment, and if they keep any part of your deposit, they must give you a written, itemized breakdown — or they lose the right to keep any of it at all.

That last point reframes the whole thing. The deposit isn't the landlord's money to divide up as they see fit and then explain to you afterward. It's your money, and New York law draws bright, specific lines around the narrow circumstances in which a landlord may keep a piece of it — lines drawn by the Housing Stability and Tenant Protection Act and the General Obligations Law. Once you know exactly where those lines fall, you can look at any deduction a landlord makes and tell, with real confidence, whether it's legitimate or whether it's an overreach you can challenge.

This guide maps those lines precisely. We'll cover the short list of what a landlord may lawfully deduct, the crucial category of "normal wear and tear" that they may not deduct for, the practices New York flatly prohibits, the itemized-statement requirement that governs any deduction, a couple of concrete scenarios showing the difference between a lawful deduction and an unlawful one, and how to challenge a deduction you believe is wrong. By the end, you'll be able to read a landlord's deduction statement the way a knowledgeable advocate would — spotting immediately what holds up and what doesn't.

One framing point to carry throughout, because it changes how you'll read everything below: the burden is on the landlord, not on you. It is not your job to prove you deserve your deposit back — the deposit is already yours, and the landlord is the one who has to justify keeping any piece of it, by fitting each deduction into a lawful category, itemizing it, documenting it, and delivering it on time. When you understand that the landlord is the one who has to satisfy the requirements, the whole exercise shifts. You're not begging for your money; you're checking whether the landlord met the conditions the law places on keeping some of it. Every rule below is a condition they have to satisfy, and every condition they fail is a piece of your deposit that comes back to you. Let's start with the short list of what they're even allowed to deduct for in the first place.

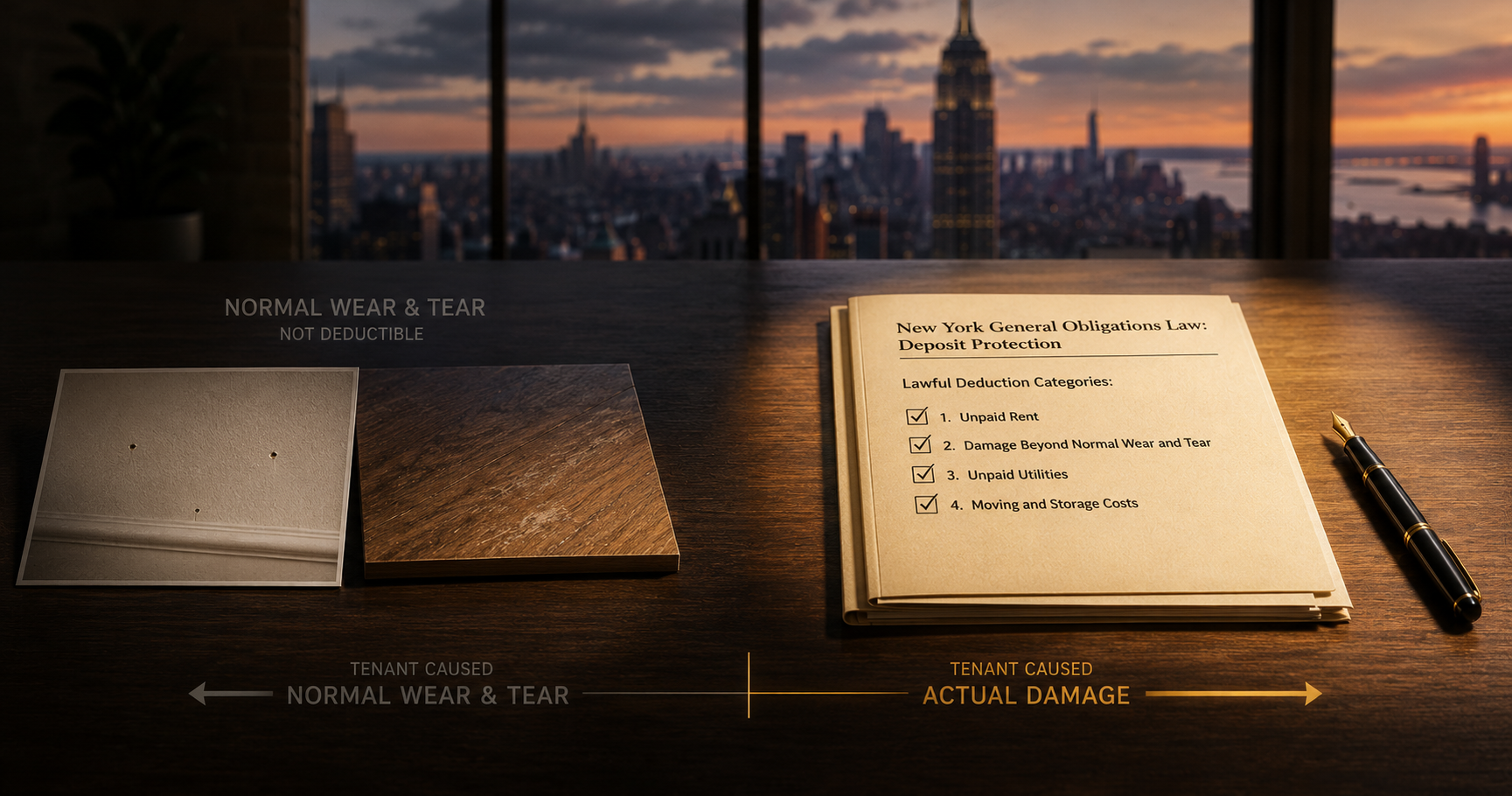

The categories a landlord may legitimately deduct from your deposit are limited, specific, and few. There are essentially four, and understanding each one — including its boundaries — is what lets you recognize when a landlord has stayed inside the lines and when they've stepped outside them.

The first is unpaid rent at the end of the tenancy. If you owe rent when you move out, the landlord can apply your deposit to that balance. This is the most straightforward category: the deposit exists in part to cover exactly this situation, so if there's a genuine unpaid rent balance, applying the deposit to it is a legitimate and expected use. The key word is genuine — the rent has to actually be owed, which means if there's a dispute about whether you owed it, or if the landlord's accounting is wrong, that's a separate question you can contest.

The second, and by far the most contested, is damage beyond normal wear and tear. This covers harm the tenant caused — actual damage — as distinct from the routine aging of an apartment. The examples that clearly fall in this category are the serious ones: big holes in walls, broken doors, smashed fixtures, carpet that's been burned or badly stained, unauthorized alterations to the unit. These are things that go beyond what ordinary living produces, and a landlord can legitimately charge to repair them. The entire weight of this category rests on that phrase "beyond normal wear and tear," which is where most deposit disputes live and which we'll examine closely in a moment, because it's the single most important line in the whole framework.

It's worth being fair and honest about this category, because a knowledgeable advocate doesn't pretend tenants are never responsible for anything. Sometimes real damage happens, and when it does, the landlord is entitled to deduct the reasonable cost of fixing it — that's what the deposit is partly for, and there's nothing improper about it. If you punched a hole in a door, or your bathtub overflow ruined the ceiling below, or you painted the living room black without permission, the landlord can legitimately charge you to set those things right. Acknowledging this isn't a weakness in your position; it's what makes you credible when you challenge the deductions that aren't legitimate. The goal is never to claim that tenants owe nothing, ever. It's to make sure you only pay for actual damage you actually caused, at a reasonable cost, properly documented — and not for the ordinary wear that the law puts squarely on the landlord.

The third is certain utilities payable directly to the landlord. If your lease specifies that you must reimburse the landlord for particular utilities, and you leave a balance owing on them, those can be itemized and deducted. Note the conditions: the lease has to actually require it, and it has to be a real balance. This isn't a general license to add utility charges; it's a narrow allowance for a specific arrangement your lease already established. If your lease says nothing about you reimbursing the landlord for utilities, a utility deduction generally has no basis at all — the landlord can't invent an obligation at move-out that the lease never created.

The fourth is reasonable moving or storage costs for belongings you leave behind. If you abandon property in the unit and the landlord has to move or store it, they can deduct the reasonable costs they actually incur doing so. Again, notice the limits built into the language: the costs have to be reasonable, and they have to be costs the landlord actually incurred — not an invented figure. This category only comes into play if you left property behind that the landlord genuinely had to deal with. A tenant who removed everything and left the unit empty gives the landlord no basis for any charge here at all; the category simply doesn't apply.

Look at that list as a whole and notice what it doesn't include. It doesn't include cleaning fees as a matter of course. It doesn't include repainting simply because it's been a few years. It doesn't include replacing carpet that wore out. It doesn't include a long list of vague charges. It doesn't include an "administrative fee," a "re-renting fee," a "turnover fee," or any of the other creative charges landlords sometimes invent. The four lawful categories are narrow and specific, and anything a landlord tries to deduct that doesn't clearly fit one of them is a deduction you have grounds to question. When you get a deduction statement, the very first thing to do is sort each line item: does this fit unpaid rent, real damage, lease-specified utilities, or abandoned-property storage? Anything that doesn't fit one of those four boxes is immediately suspect, before you even get to questions of documentation or timing.

Here is the concept that decides more deposit disputes than any other, and the one landlords most often exploit when they assume a tenant doesn't know the rules: normal wear and tear. It is the ordinary, minor deterioration that happens simply from living in a unit — and landlords cannot lawfully deduct for it. Not for any of it. Understanding this category clearly is the single most valuable thing you can take from this guide, because it's the basis on which a huge share of improper deductions can be challenged.

Think about what "normal wear and tear" actually means. An apartment that has been lived in — even carefully, even respectfully — does not come out the other end looking brand new, and the law does not expect it to. Ordinary life leaves ordinary marks, and those marks are the landlord's responsibility to address between tenants, as a normal cost of renting property, not something to charge back to the person who simply lived there. The typical examples make the category concrete. Paint that has faded or become slightly scuffed from time and everyday use is normal wear and tear. Minor scuffs on hardwood floors from regular foot traffic are normal wear and tear. Carpet that's worn in the high-traffic areas, or linoleum with light wear, is normal wear and tear. Small nail holes from hanging pictures, or a door handle that's become slightly loose over the years — these too are normal wear and tear. None of them is damage. All of them are the expected signature of ordinary occupancy, and none is a lawful basis for keeping your deposit.

The reason this matters so much is that these are precisely the things landlords most often try to charge for, because they happen in nearly every apartment and because a tenant who doesn't know better might assume the charge is legitimate. A landlord keeps a chunk of the deposit for "repainting," when the paint just needed the ordinary refresh that years of normal living call for. A landlord charges for "carpet replacement," when the carpet simply wore out from being walked on. A landlord deducts for "cleaning and touch-ups" that amount to nothing more than the routine preparation any unit needs between tenants. Each of these is a landlord trying to shift their own ordinary cost of doing business onto your deposit, dressed up in the language of "damage." And each of them is challengeable.

Here's the good news about challenging them: normal wear and tear is exactly the kind of thing your documentation can prove. If a landlord claims faded paint or worn carpet as "damage," you can counter with photos, videos, and move-in and move-out inspection notes showing the actual condition. A dated move-out video showing carpet that's merely worn rather than stained or burned directly refutes a "carpet damage" charge. Photos showing walls with nothing more than small nail holes and ordinary scuffs refute a claim of wall "damage." The distinction between wear and damage isn't a matter of opinion that the landlord gets to decide by asserting it — it's a factual question your evidence can answer, and when your evidence shows ordinary wear, the deduction doesn't hold. This is why the documentation habit matters so much, and why the tenant who photographs their unit at move-out holds the power to defeat exactly these kinds of improper charges.

If you're ever unsure which side of the line a particular condition falls on, a useful test is to ask what caused it: did it result simply from ordinary, careful use over time, or from something beyond that — an accident, misuse, neglect, or deliberate alteration? Carpet worn thin in the path between the door and the couch was caused by nothing but walking, which is exactly what carpet is for; that's wear. A cigarette burn or a wine stain the size of a dinner plate was caused by a specific mishap; that's damage. Paint that dulled and yellowed over four years was caused by time and air; that's wear. A wall with a fist-sized hole was caused by an impact; that's damage. The cause tells you the category. And notice which way the ambiguous cases tend to break: the longer you lived in the unit, the more deterioration counts as normal, because more wear is expected from longer occupancy. A landlord charging a four-year tenant for worn carpet is on especially weak ground precisely because four years of use is supposed to wear carpet. Time is on the tenant's side here — the same condition that might look borderline after six months reads as plainly normal after several years.

Beyond the wear-and-tear line, New York law draws several other bright lines around what landlords simply cannot do with your deposit — prohibitions written into the Housing Stability and Tenant Protection Act and the General Obligations Law. These aren't gray areas or matters of interpretation. They're flat rules, and a landlord who crosses any of them is violating the law.

A landlord cannot charge more than one month's rent total as a deposit or up-front "security." This is a hard cap, and it can't be evaded by relabeling. Extra "last month's rent," pet deposits, key deposits, or move-in fees that function as security cannot be used to push the total above one month's rent. So if a landlord collected a month's security plus a pet deposit plus a "move-in fee" that together exceed one month's rent, the excess very likely violates the cap regardless of what each piece was called. The law looks at the substance — money held as security — not the labels a landlord attaches to it.

This anti-relabeling principle is worth understanding well, because creative labeling is exactly how landlords try to slip past the cap. The law's focus on substance over label means you should add up everything a landlord collected that functions as security or a refundable holding of your money, not just the item explicitly called "security deposit." A "pet deposit" is still a deposit. A "key deposit" is still a deposit. A "move-in fee" that's really just security by another name still counts. If the total of all these, taken together, exceeds one month's rent, you have a cap violation on your hands even though no single line item did. Landlords who want more than a month of security sometimes try to break it into pieces with different names, betting that a tenant will see each piece as a separate, legitimate charge. Adding them up and comparing the total to one month's rent is how you catch that, and the excess is money you can generally demand back.

A landlord cannot label any part of the deposit as "non-refundable." This one catches many tenants off guard, because non-refundable fees appear in leases all the time. But any clause that makes your deposit, or a "cleaning fee," automatically non-refundable violates New York law. The whole nature of a security deposit is that it's your money, returnable except to the extent the landlord has a lawful basis to keep some of it. A landlord cannot convert it into their money by simply writing "non-refundable" into the lease. If your lease contains such a clause, it's not enforceable, and the fact that you "agreed" to it doesn't make it lawful — the law voids the practice regardless of what you signed. This is a crucial point, because tenants often assume that a signed lease is binding in all its terms, and so they never question a "non-refundable cleaning fee" they agreed to at move-in. But you cannot validly agree to give up a protection the law refuses to let you waive. That "non-refundable" cleaning fee is refundable in the sense that matters: the landlord can only keep money from it for actual, lawful, itemized deductions, exactly as with the rest of your deposit. The label doesn't change the law.

A landlord cannot keep money for normal wear and tear. We covered why in the previous section, but it bears listing among the flat prohibitions, because it's not merely that wear-and-tear charges are weak — retaining a deposit for routine aging or minor cosmetic issues is expressly prohibited. It's a rule, not a suggestion.

A landlord cannot use your deposit during the tenancy without your consent. Your deposit is held in trust until the tenancy ends; the landlord doesn't get to dip into it mid-lease to cover a rent shortfall or anything else, helping themselves to your money before you've even moved out. Unless you clearly agree otherwise in writing, that money stays untouched until the tenancy is over. A landlord who "borrows" from your deposit during the lease is misusing funds they're only supposed to be holding in trust, not spending, until the tenancy is over.

And a landlord cannot ignore the 14-day rule — which may be the most powerful protection of all. Within 14 days after you vacate, the landlord must either return your full deposit or send you an itemized list of deductions along with any remaining balance. One or the other, within 14 days. And here's the teeth: if they miss this deadline, or fail to send the itemization, they forfeit any right to keep the deposit — even if there was real damage. Read that carefully, because it's remarkable. A landlord could have a legitimate claim for actual damage, and still lose the entire right to deduct for it, simply by blowing the 14-day deadline or failing to itemize properly. The law cares so much about tenants getting a prompt, transparent accounting that it penalizes the failure to provide one by wiping out the landlord's deductions altogether. This means the deadline itself is a basis for recovering your full deposit, independent of the merits of any particular charge.

Think about how this interacts with everything else in this guide, because it's a kind of master key. Most of the deduction rules require you to examine the substance of a charge — is this wear or damage, is this cost reasonable, is this category lawful. But the 14-day rule doesn't require you to win any of those substantive arguments. If the landlord simply didn't return your deposit or send a proper itemized statement within 14 days of your move-out, you may be entitled to the entire deposit back on that basis alone, without ever having to debate whether the carpet was worn or damaged. This is why tracking your exact move-out date and counting 14 days forward matters so much: the deadline gives you a clean, powerful claim that sidesteps every messier argument. Many deposit cases are won not by proving the landlord's charges were wrong, but simply by showing the landlord never provided the timely, itemized accounting the law requires. It's the simplest violation to prove — a date passed, and nothing arrived — and one of the most decisive.

The itemized statement sits at the center of this entire framework, because it's the mechanism that forces a landlord's deductions into the open where they can be examined. If a landlord keeps any part of your deposit, they must give you a written, itemized statement — and understanding what that statement has to contain lets you judge whether the landlord has actually complied or just gone through the motions.

A proper itemized statement has to show the specifics: the repair costs, any utility charges payable to the landlord, any outstanding rent, and any moving or storage costs for your possessions — each broken out, not lumped together. The point of itemization is transparency: you're entitled to see exactly what you're being charged for and why, category by category, dollar by dollar. A statement that just says "deducted $900 for damages" isn't a proper itemization; it's a vague assertion that fails the requirement. The law wants line items, not lump sums.

And those line items should line up with reality — with actual invoices and receipts, not vague, round numbers. This gives you a specific tool: you can demand copies of the repair receipts or estimates behind the deductions, to test whether they're reasonable and real. A landlord who charges "$500 for repairs" but can't produce a single invoice or estimate for that work has given you strong grounds to challenge the deduction, because the round number with no documentation behind it looks exactly like what it often is — a figure pulled from the air rather than a real cost incurred. Suspiciously round numbers, charges with no receipts, estimates that never materialize into actual invoices: these are the signatures of deductions that won't hold up, and you're entitled to probe them.

The reasonableness requirement is worth emphasizing alongside the reality requirement, because a deduction can be for genuine damage and still be improper if the amount is inflated. A landlord can only deduct the reasonable cost of repairing actual damage, not whatever figure they'd like to charge. If you genuinely cracked a tile and the landlord bills you $800 for what any reasonable repair would cost $150, the excess is not a lawful deduction even though the underlying damage was real. This is another reason to demand the receipts: they let you check not just whether the work happened, but whether the cost was reasonable. A padded invoice, a charge for replacing an entire floor when a single tile needed fixing, a "repair" cost that suspiciously equals the exact amount of your remaining deposit — these are signs of a landlord inflating a real deduction into an unlawful one. You're entitled to a repair charge that reflects the reasonable cost of fixing what was actually damaged, and nothing more.

Then there's the ultimate backstop, which we've touched on but which belongs here too, because it's tied directly to the itemization requirement: if the landlord does not provide an itemized statement at all, New York law treats that failure as a forfeiture of their right to keep the deposit at all. No itemization, no deductions — full stop. The itemized statement isn't optional paperwork the landlord can skip when it's inconvenient. It's the condition on which their entire right to keep any of your money depends. A landlord who keeps your deposit and sends you nothing, or sends a vague non-itemized note, hasn't just been sloppy; they may have forfeited the right to keep a cent, which means you can demand the whole deposit back regardless of the underlying facts.

The difference between a lawful deduction and an unlawful one becomes vivid when you see it in a concrete case, so let's walk through two — one of each — because the contrast makes the rules easy to apply to your own situation.

First, a lawful deduction. Suppose you accidentally broke a bathroom sink during your tenancy, and you also owed half a month's rent when you moved out. After you leave, the landlord sends you an itemized letter within the 14-day window: $400 for the sink replacement and $750 for the unpaid rent, with the receipts for the sink work attached, and a check for the remaining balance of your deposit. Walk through why this is generally allowed. The sink is actual damage beyond normal wear and tear — a broken fixture, not ordinary aging — so it fits a lawful deduction category. The unpaid rent is a genuine balance, another lawful category. The landlord itemized each charge specifically, backed the repair with a receipt, met the 14-day deadline, and returned the balance. Every box is checked. This is what a lawful deduction looks like: real charges in permitted categories, documented, itemized, and returned on time. When a landlord does all of that, the deduction generally stands, and that's the system working as intended.

Now, an unlawful deduction. Suppose you lived in the unit for four years, and at move-out the carpet simply looks worn — no burns, no stains, just the natural result of four years of being walked on. The landlord keeps your entire deposit, citing "old carpet," and never sends an itemized list within 14 days. Walk through everything wrong here. Worn carpet after four years of ordinary use is textbook normal wear and tear, which is not a lawful deduction at all — the landlord is charging you for the routine aging they're supposed to absorb. And on top of that substantive problem, they missed the 14-day deadline and never sent an itemization, which by itself forfeits their right to keep any of the deposit. So this landlord has committed two independent violations: an improper wear-and-tear charge, and a blown deadline with no itemization. Either one alone would entitle you to push back; together, they make your position very strong. You can demand the full deposit back, and if the landlord refuses, you can pursue it — with a certified demand letter, the Attorney General's mediation, or small claims court — from a position of real strength.

Put the two scenarios side by side and the framework becomes second nature. Lawful: actual damage or genuine unpaid rent, in a permitted category, itemized with documentation, delivered within 14 days. Unlawful: normal wear and tear dressed up as damage, or a missed deadline, or a vague non-itemized statement, or charges with no receipts behind them. Once you can sort a landlord's deductions into those two buckets, you know exactly where you stand and exactly what you can challenge.

Knowing a deduction is improper is one thing; pushing back on it effectively is another, and the good news is that the deduction framework itself hands you the tools. Because a landlord's deductions have to fit specific categories, be itemized, be documented, and arrive on time, each of those requirements is also a place you can apply pressure. Challenging a bad deduction isn't about arguing over feelings; it's about holding the landlord to the specific rules their deduction has to satisfy.

The first move, when you receive a deduction you doubt, is to demand the supporting documentation in writing. You're entitled to test whether the deductions are real and reasonable, and the way you do that is to ask for the receipts, invoices, or estimates behind each charge. This request is quietly powerful, because it separates real deductions from invented ones instantly. A landlord who actually replaced a damaged fixture can produce the invoice; a landlord who pulled "$500 for repairs" out of the air to shave your deposit cannot. When you put the request in writing — "please provide copies of the receipts, invoices, or estimates supporting each deduction listed in your statement" — you force the issue. Either the documentation appears, in which case you can assess whether it's genuine damage and a fair cost, or it doesn't, in which case you've exposed a deduction that likely can't survive scrutiny.

The second move is to match each deduction against the rules and name the specific problem with the ones that fail. This is where your knowledge of the framework does the work. For each questionable charge, identify precisely why it's improper: "The $600 carpet charge is for normal wear and tear from four years of ordinary use, which is not a lawful deduction." "The 'cleaning fee' is labeled non-refundable in the lease, which New York law prohibits." "No itemized statement was provided within 14 days, which forfeits the right to keep any of the deposit." Naming the specific rule violated is far more effective than a general complaint that the deductions feel unfair, because it shows the landlord — and later, if needed, a mediator or a judge — that you know exactly which line was crossed. A landlord who receives a letter identifying the precise legal defect in each deduction is dealing with a tenant who is clearly prepared to enforce the rules, which often prompts them to return the money rather than fight a losing battle.

The third move, if the landlord won't correct an improper deduction, is to escalate — and here the deduction question connects to the broader recovery process. You can send a formal certified demand letter citing the specific violations, you can file a complaint with the New York Attorney General's office, which offers mediation for deposit disputes, and you can bring a case in small claims court, where in New York City you can sue for up to $10,000 without a lawyer. Your documentation is what carries you through: the dated move-out photos and video that prove ordinary wear rather than damage, the lease, the landlord's own deduction statement, and the record of your demand for receipts. The clarity of New York's deduction rules works in your favor at every stage, because you're not arguing an ambiguous point — you're showing that specific, well-defined rules were broken. And remember that willful, bad-faith withholding can expose a landlord to penalties beyond the deposit itself, which is one more reason many landlords choose to correct an improper deduction once a tenant pushes back knowledgeably.

The throughline across all three moves is that a deduction is a claim, not a decision. The landlord is asserting they're entitled to keep a piece of your money, and every element of that assertion — the category, the itemization, the documentation, the timing — is something you can test and, where it fails, defeat. You don't have to accept a deduction just because it's written on a statement. You get to hold it to the standard the law sets.

Step back and look at what you can now do that most tenants can't: read a landlord's deduction statement and know, line by line, what's legitimate and what's overreach. You know the four lawful categories — unpaid rent, real damage beyond wear and tear, certain lease-specified utilities, and reasonable storage of abandoned property — and you know that anything outside them is questionable. You know that normal wear and tear, the faded paint and worn carpet and small nail holes of ordinary living, is expressly not deductible, and that your photos and inspection notes can prove it. You know the flat prohibitions: no more than one month total, nothing labeled "non-refundable," no dipping into the deposit mid-lease, and no ignoring the 14-day rule. And you know that the itemized statement is the landlord's make-or-break obligation — vague numbers invite a demand for receipts, and no itemization at all forfeits their right to keep anything.

Here's the reframe to carry out of all this. A deposit deduction can feel like a verdict the landlord hands down and you simply have to accept — they kept what they kept, and who are you to argue? But that's not the relationship the law creates. The landlord doesn't get to decide what's fair and inform you afterward. They're operating inside a narrow set of rules, and every deduction they make is a claim that has to fit those rules — a claim you're fully entitled to test against the categories, against the wear-and-tear line, against the documentation requirement, against the deadline. You're not a supplicant hoping for the landlord's fairness. You're a reader of a statement that either complies with the law or doesn't, and you now know how to tell the difference.

So when your deposit comes back short, don't just absorb it. Read the statement against everything here, running through a quick checklist for each deduction. Does it fit one of the four lawful categories, or is it disguised wear and tear or an invented fee? Is it itemized specifically, or lumped into a vague total? Is it documented with a real receipt, or a round number pulled from the air? Is the amount reasonable, or inflated past what the repair would actually cost? And did the whole statement even arrive within 14 days, or not at all? Each of those questions is one you can now answer, and each one is a place a landlord's overreach can be caught and challenged — with a written demand for receipts, a letter naming the specific violation, and, if needed, mediation or small claims court.

The deposit was your money to begin with, and the law only lets the landlord keep a narrow, specific, documented, timely slice of it. Everything about the framework points in the same direction: the categories are few, the wear-and-tear exclusion is broad, the documentation requirement is strict, and the deadline is unforgiving — all of it designed to make sure a landlord can't quietly keep money they aren't entitled to. Anything beyond that narrow lawful slice is yours to demand back, and now you know exactly how to tell where the slice ends and your money begins. Find out what you're really owed.