Your security deposit is your money. That single fact gets lost more often than almost anything else in renting, because the deposit sits in the landlord's hands for the length of your tenancy, and possession has a way of feeling like ownership. But it isn't the landlord's money — it's yours, held under rules that New York law spells out in unusual detail. The state strictly limits how much a landlord can collect, dictates how the deposit must be held, narrows what can lawfully be deducted from it, and sets a hard deadline for getting it back. And when a landlord breaks any of those rules — charges too much, raids the deposit for things they're not allowed to, or simply fails to return it on time — you have clear, usable remedies, in court and through state authorities.

This is a guide to those rights, laid out plainly so you know exactly what the law guarantees you and exactly what to do when a landlord ignores it. We'll cover how much a landlord can collect, how your deposit must be held, what can and can't be deducted, the inspection and return deadlines that protect you, and the remedies available when the rules are broken. The throughline is simple and worth holding onto from the start: the deposit is yours, the law is detailed and largely on your side, and a landlord who treats your deposit as a discretionary slush fund is usually breaking rules you can enforce. Let's go through what those rules actually are.

One reason this knowledge is so valuable is that the deposit is, for many tenants, one of the largest single sums of money in their financial life at any given moment — often a full month's rent sitting in someone else's hands. Losing it unjustly isn't a minor annoyance; it can mean not being able to afford the deposit on the next place, which is how a wrongful deposit retention quietly traps people in housing limbo. That's precisely why New York wrote such detailed rules around it, and why knowing those rules pays off so directly. The landlord who assumes you don't know the law is counting on exactly that — that you'll accept a vague deduction, miss the significance of a blown deadline, or never realize you were overcharged at move-in. Knowing the framework removes that advantage. Each rule below is something you can check your own situation against, and each one a landlord violates is leverage in your hands.

Start with the amount, because this is where some of the most common overreach happens — and where New York drew one of its brightest lines. For residential rentals statewide, a landlord generally cannot charge more than one month's rent as a security deposit or advance. That's the cap. Not two months, not a month-and-a-half, not whatever the market will bear. One month's rent is the ceiling for most tenancies, full stop.

This cap directly forbids a practice that used to be routine: demanding "last month's rent" on top of a one-month security deposit. A landlord cannot require both — they cannot stack an extra month of "last month's rent" on top of a full month's security deposit for most tenancies. The total upfront security a landlord can hold is capped at that one month, which means the old move of asking for first month, last month, and a security deposit — effectively three months up front just to move in — is no longer lawful for most rentals. If a landlord is demanding that kind of package, they're very likely demanding more than the law allows.

This cap matters for more than just the dollars at move-in, though those dollars are significant — the difference between one month and three months up front can be the difference between being able to take an apartment and being priced out of it entirely. The cap exists in part precisely to lower that barrier, so that the upfront cost of moving doesn't become an insurmountable wall, especially for tenants without large savings. But it also matters because an over-limit deposit is itself a violation you can act on. If a landlord collected more than one month, that excess wasn't lawful to demand, and you generally have the right to get the unlawful portion back. So the cap isn't only a shield against being overcharged at the start; it's also a basis for recovery if you were overcharged and didn't realize it at the time. Tenants who paid an unlawful "first, last, and security" package years ago sometimes don't recognize until later that part of what they handed over was never lawfully owed.

This one-month cap comes from the Housing Stability and Tenant Protection Act of 2019, the same sweeping reform that strengthened so many tenant protections in New York, and it governs most modern leases as the baseline. There are special rules for rent-regulated apartments, which can have their own framework, so the picture for a rent-stabilized unit may differ — but for the typical market-rate tenancy, the one-month cap is the rule to know. A concrete illustration makes the line unmistakable: if your monthly rent is $1,500, a landlord cannot legally demand a $3,000 "security plus last month" package. The maximum lawful deposit is $1,500 — one month — and that single month is what must be handled according to all the rules that follow. So before you even get to how a deposit is held or returned, check the threshold question: did the landlord collect more than one month to begin with? If they did, that itself may be unlawful.

Here's something many tenants never realize: a landlord doesn't just get to pocket your deposit and spend it. New York law dictates how the money must be held, and in larger buildings the requirements are strict — because the deposit isn't the landlord's money to use, it's your money in their safekeeping.

In buildings with six or more units, the landlord must place your deposit in a separate, interest-bearing account at a New York bank, and — this is the crucial concept — the landlord acts as a trustee of that money, not its owner. A trustee holds money on behalf of someone else and is bound to handle it accordingly; they can't treat it as their own funds, can't commingle it with their personal or business money, and can't spend it. So in these larger buildings, your deposit isn't supposed to be floating around in the landlord's general account or funding their operations. It's supposed to be sitting in a dedicated bank account, segregated, with your name effectively attached to it, while the landlord merely holds the key.

That trustee arrangement comes with obligations that benefit you directly. The landlord must tell you the name and address of the bank where your deposit is held — you're entitled to know where your money is. And because the account is interest-bearing, the landlord must pay you the annual interest it earns, minus an administrative fee of up to 1% of the deposit. So your deposit isn't just sitting safely; in these buildings it's earning interest that belongs to you, less only that capped 1% the landlord may keep for administration. If you've never received an interest payment or been told which bank holds your deposit in a building of this size, those are signs the landlord may not be following the rules.

Why does the law go to the trouble of requiring a separate account and a trustee relationship, rather than just trusting landlords to give the money back? Because the segregation is what protects the money's existence. If a landlord were allowed to drop your deposit into their general operating account and spend it on the building's expenses or their own, then when the time came to return it, the money might simply not be there — gone into a mortgage payment or a contractor's bill, with nothing left to give back. Keeping the deposit in a separate, dedicated account ensures it remains intact and available, genuinely held rather than spent. The trustee concept reinforces this legally: a trustee who raids the trust isn't just breaching a contract, they're violating a duty of a more serious kind. For you, the practical upshot is reassuring — in a building of six or more units, your deposit is supposed to exist as actual, segregated, identifiable money in a named bank, not as an IOU the landlord hopes to cover later. That's a meaningfully stronger protection than simply being owed the amount, and it's worth knowing you're entitled to it.

The protections also follow the money when a building changes hands. If the building is sold, the seller must either transfer the deposits to the new owner or return them to the tenants — the deposits can't simply vanish in the transaction. And the new owner becomes directly responsible for returning deposits and interest in many situations, whether or not they actually received the money from the seller. That last point is important and easy to miss: a new landlord generally can't tell you "the previous owner kept your deposit, so it's not my problem." In many situations the law makes the new owner answerable for returning your deposit regardless, which protects you from being caught in the gap between a seller and a buyer pointing fingers at each other. Your deposit is meant to be protected through the sale, not lost in it.

This protection addresses a trap that would otherwise be devastating, and tenants are often relieved to learn it exists. Buildings change ownership all the time, and a tenant who handed their deposit to a landlord three years ago may be dealing with an entirely different owner by the time they move out. Without this rule, that tenant would be horribly exposed: the original landlord who holds the deposit is gone, and the new owner could disclaim any responsibility for money they say they never received. The law closes that gap by making the deposit obligation run with the building in many situations, so that the current owner — the one you're actually dealing with at move-out — is the one who has to return it. You don't have to track down a former landlord who sold the building and disappeared, and you don't have to absorb the loss because two owners failed to handle the transfer properly between themselves. That's their problem to sort out, not yours. As far as your right to your deposit is concerned, the law aims to keep it intact and recoverable no matter how many times the building has been bought and sold during your tenancy.

This is the area where most disputes erupt, because it's where a landlord decides how much of your deposit to actually give back. New York narrows their discretion sharply: the categories a landlord may lawfully deduct from are limited, specific, and short. They are unpaid rent, the cost of repairing damage you caused beyond normal wear and tear, certain utility charges payable to the landlord, and the reasonable costs of moving or storing property you abandoned. That's essentially the complete list. A deduction that doesn't fit one of those categories is a deduction the landlord generally isn't entitled to make.

The single most important phrase in that list is "beyond normal wear and tear," because it's where landlords most often overreach and tenants most often get shortchanged. Normal wear and tear — the ordinary aging of a lived-in apartment — cannot justify keeping your deposit. Faded paint, minor scuffs on the floors from everyday use, carpet that's worn from being walked on: these are the expected results of someone living in a home, not damage, and a landlord can't charge you for them. The law draws a clear line between the normal deterioration that comes from ordinary use, which is the landlord's cost of doing business, and actual damage beyond that, which is yours. So when a landlord tries to deduct for repainting a wall that just needed repainting after years of normal living, or for carpet that simply wore out, they're reaching past what the law allows. Your deposit is not supposed to fund the routine refreshing of an apartment between tenants.

The distinction is worth understanding well, because landlords count on tenants not knowing where the line falls. Think of it this way: wear and tear is what happens to an apartment simply because a human being lived in it carefully for a period of time. Paint dulls. Floors lose their shine in the walking paths. Carpet flattens. Small nail holes appear where pictures hung. These are the inevitable, gradual effects of ordinary occupancy, and the landlord is expected to absorb them as a normal cost of renting — refreshing the unit between tenants is part of being a landlord, not something tenants pre-pay through their deposits. Damage, by contrast, is harm beyond that ordinary baseline: a large hole punched in a wall, a cracked window, a carpet stained or burned, a fixture broken through misuse. That's the category a landlord can legitimately charge against your deposit. The test isn't "does the apartment need any work before the next tenant?" — almost every apartment does. The test is whether the condition goes beyond what normal, careful living produces. A great many wrongful deductions collapse the moment you hold them up to that standard, because so much of what landlords try to charge for — the repaint, the worn carpet, the general "freshening up" — is precisely the normal wear and tear the law says is on them, not you.

And when a landlord does keep any part of your deposit, they don't get to do it silently or vaguely. They must give you an itemized, written statement of exactly what they deducted and why — the repairs, the rent, the utilities, the storage, each spelled out. Not a lump "deducted for damages," but an actual itemization. This requirement matters enormously, because vague deductions are how landlords get away with unjustified ones, and the itemization requirement forces them into the open where their claims can be examined.

Here's the part that gives that requirement teeth: if a landlord fails to provide that itemized written statement, they can forfeit the right to keep any of the deposit at all. Read that carefully, because it's a powerful protection. The itemization isn't optional paperwork the landlord can skip if it's inconvenient. It's a condition of keeping any of your money. A landlord who just holds onto your deposit without giving you a proper itemized statement may, by that failure alone, lose the right to deduct anything — meaning they owe you the whole deposit back regardless of what they thought they could keep. The law put the burden squarely on the landlord to justify, in writing, every dollar they withhold, and built a real penalty into their failure to do so.

There's an even sharper consequence for the worst cases. New York law provides that a landlord who willfully violates the deposit rules can be liable for punitive damages of up to twice the amount of the deposit, on top of returning what they wrongfully kept. Think about what that means for the landlord who keeps your deposit not through some honest dispute about a repair but out of bad faith — because they assume you won't fight, or simply want to keep the money. That willful, bad-faith retention isn't a costless gamble for them. It exposes them to owing you potentially three times the deposit in total: the wrongfully withheld amount returned, plus up to double that as a penalty. So the deposit rules aren't just guidelines a landlord can ignore and, at worst, be made to comply with later. A landlord who flouts them in bad faith risks paying substantially more than they tried to keep — which is exactly why a tenant who knows these rules holds more leverage than they might assume. The same retention the landlord imagined as easy money can become an expensive mistake.

New York doesn't just govern what happens to your deposit after you leave — it gives you a tool to protect it before you go, and then sets a hard clock on its return. Both of these are protections tenants frequently don't know they have, and using them can be the difference between getting your deposit back smoothly and fighting for it afterward.

The tool before move-out is the pre-move-out inspection, and it's your right to request. You can ask for an inspection of the apartment before your tenancy ends, and you have the right to be present for it. The timing is specified: the inspection must occur no earlier than two weeks and no later than one week before your move-out date, and the landlord must give you at least 48 hours' written notice of the date and time. So this isn't a vague courtesy — it's a structured right with defined timing. And here's why it's so valuable: after the inspection, the landlord must give you a written list of the issues they plan to deduct for, which gives you the chance to fix those things yourself before you leave. That advance list is the opposite of the surprise deduction. Instead of moving out and discovering weeks later that the landlord is charging you for a list of things you never saw, you find out beforehand, while you still have access and time, and you can address them — clean the thing, repair the small thing — so they can't be charged against your deposit at all. Requesting the inspection turns the deduction process from an ambush into something you can get ahead of.

It's worth dwelling on just how much leverage this one right hands you, because it's among the most underused protections in the entire deposit framework. Most deposit disputes happen after the tenant has moved out and lost all access to the apartment — the tenant is gone, the keys are returned, and the landlord unilaterally decides what to charge, leaving the tenant to fight about it from the outside with no ability to fix anything. The pre-move-out inspection flips that timing entirely. By forcing the landlord to tell you, in writing, before you leave, what they intend to deduct for, it gives you a window in which you still hold the keys and can act. If the landlord lists a dirty oven, you clean the oven. If they list a small hole, you patch it. Each item you cure is an item that can't appear on the final deduction list. You're effectively getting a preview of the landlord's deduction case while you still have the power to dismantle it. The catch is that you generally have to request the inspection to trigger this right, so it only protects the tenants who know to ask — which now includes you. As your move-out approaches, putting in that request is one of the highest-value, lowest-effort things you can do to protect your deposit.

Then comes the return deadline, which is strict. When you vacate and return the keys on time, the landlord must return the balance of your deposit — minus any lawful, itemized deductions — within a defined statutory period: 14 days under current statewide New York law. Fourteen days. Not "eventually," not "when they get around to it," not "after they've finished some renovation." Within fourteen days of your moving out and returning the keys, the deposit balance must be back to you, accompanied by the itemized statement if they're keeping any of it. This deadline is one of your strongest protections, because it converts the vague anxiety of "will I ever see my deposit again?" into a concrete date by which the law requires action. If fourteen days pass and you've received neither your deposit nor a proper itemized statement, the landlord is out of compliance — and as we've seen, the failure to itemize can cost them the right to keep any of it.

It helps to put the rules together in a single concrete picture, because seen as a sequence they're far clearer than as a list. Say your rent is $1,500 a month. At move-in, the most a landlord can lawfully collect as security is $1,500 — one month — and they cannot tack on an additional "last month's rent" to make it $3,000. If you're in a building with six or more units, that $1,500 must go into a separate interest-bearing account at a New York bank, you must be told which bank holds it, and you're owed the annual interest minus up to 1%. During your tenancy, the deposit sits there as your money in the landlord's trust, not theirs to spend.

When you're ready to leave, you can request a pre-move-out inspection, to happen between two weeks and one week before you go, with 48 hours' written notice, and you can be present. Afterward, the landlord gives you a written list of anything they intend to deduct for, and you get the chance to fix those items before you hand back the keys. Once you vacate and return the keys on time, the landlord has 14 days to return your $1,500 — less only lawful, itemized deductions for things like unpaid rent or actual damage beyond normal wear and tear, each spelled out in writing. If they keep some of it, you get an itemized statement explaining exactly why. If they keep it without that statement, they may forfeit the right to keep any of it. That's the full lifecycle of a deposit handled lawfully, and at every stage the law is specific about what protects you. When a landlord's behavior departs from that picture — a bigger deposit demanded, no bank disclosed, a vague deduction, a missed deadline — you can see the departure clearly, because you now know what the lawful version looks like.

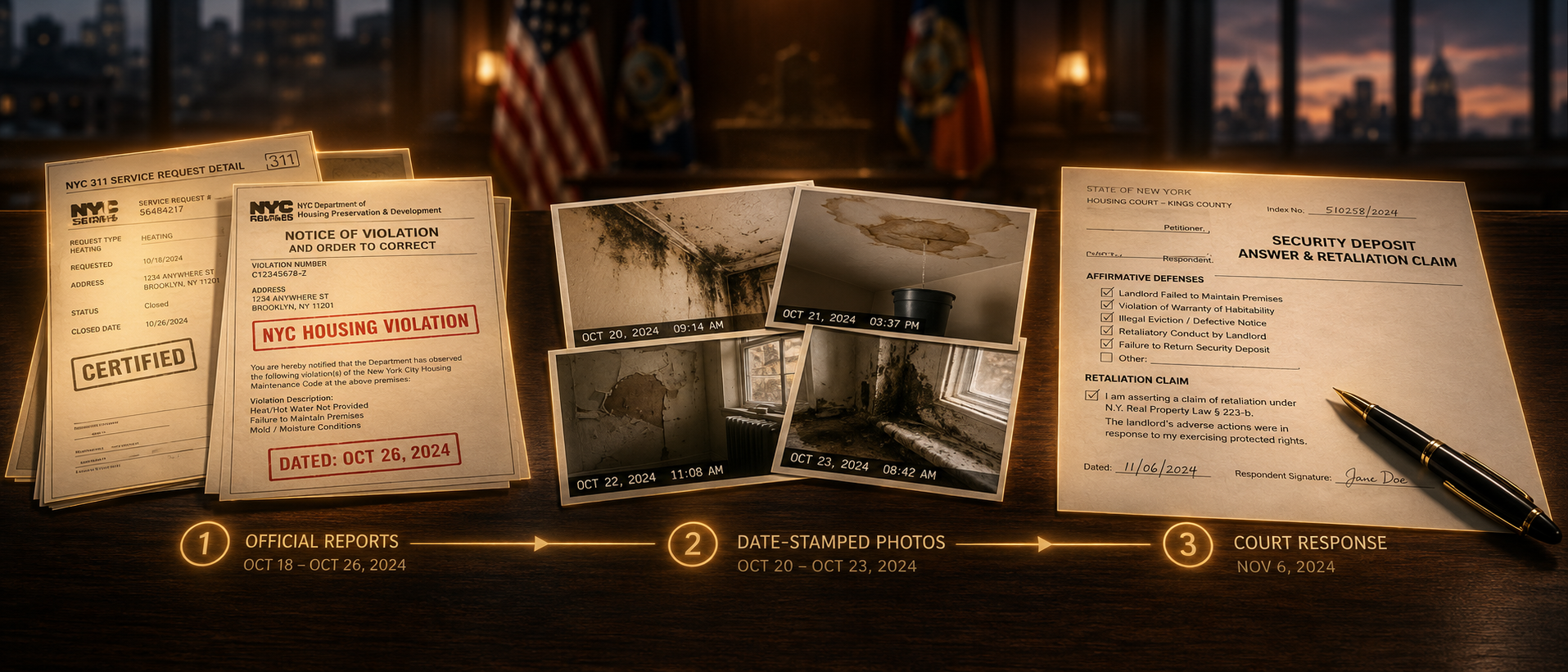

The framework is clearest when you watch it catch an actual violation, so let's follow a realistic dispute through. Imagine a tenant who paid a $1,500 deposit, lived in the apartment for three years, kept it reasonably, and moved out on time, handing back the keys. Three weeks pass. No deposit arrives, no statement, nothing. When the tenant finally reaches the landlord, they're told the entire $1,500 was kept "for repainting and cleaning and general wear on the place."

Look at how many of the rules that single response runs into. First, the timing: more than 14 days have passed with no return and no itemized statement, so the landlord is already out of compliance with the deadline. Second, the itemization: "repainting and cleaning and general wear" is not an itemized written statement specifying each deduction and its basis — it's a vague lump justification, exactly what the law forbids. Third, the substance: repainting after three years of living and "general wear" are textbook normal wear and tear, which cannot lawfully be charged to the deposit at all. And the failure to provide a proper itemized statement carries its own consequence — the landlord may forfeit the right to keep any of the deposit on that basis alone.

Now watch the tenant use the framework. They send a written demand for the full $1,500, citing that no itemized statement was provided within 14 days and that the claimed deductions are normal wear and tear, not lawful deductions. They attach dated move-out photos showing the apartment in good condition. The landlord, faced with a tenant who clearly knows the rules and has evidence, may simply pay rather than risk a losing fight. If the landlord still refuses, the tenant files in small claims court for up to $10,000, brings the lease, the photos, and proof of on-time move-out, and relies on Article 7 of the General Obligations Law — and walks in with a strong case: a missed deadline, no valid itemization, and deductions that aren't legitimate. The same dispute, run by a tenant who didn't know the rules, ends with a shrug and a lost $1,500. Run by a tenant who does, it ends with the deposit recovered — and possibly interest on top. The difference is entirely in knowing what the lawful version looks like and being able to point to each place the landlord departed from it.

Knowing your rights is only half the picture; the other half is knowing what to do when a landlord violates them, because rights without remedies are just wishes. New York gives you real, usable remedies, escalating from a simple written demand all the way to court — and the good news is that the strongest tool, small claims court, is built for exactly this and doesn't require a lawyer.

Start with a written demand and your evidence. If a landlord is withholding your deposit unlawfully, demand it back in writing, and keep copies of everything that supports your case: the lease, any move-in or move-out inspection reports, photos of the apartment's condition, receipts, and your communications with the landlord. This documentation is what proves you paid your rent and left the unit in good condition, and it's what turns "the landlord says I damaged the place" into "here are dated photos showing I didn't." A written demand sometimes resolves matters on its own, because a landlord who realizes you know your rights and have evidence may simply return the deposit rather than fight. And if it doesn't resolve things, you've created a record and built your file for the next step.

The most valuable evidence is often created at the very beginning and the very end of a tenancy, before any dispute exists — which is why the smartest move is to document defensively from day one. When you move in, photograph or video the apartment's condition thoroughly, with dates, capturing any pre-existing wear or damage so it can never be blamed on you later. Keep those move-in photos somewhere safe for the entire length of your tenancy. Then, when you move out, do the same: a full set of dated photos and video showing the condition you left the place in. This bookending is enormously powerful in a deposit dispute, because it lets you show, side by side, the condition at the start and the condition at the end — which directly answers any claim that you caused damage. A landlord asserting you wrecked the carpet has a hard time when you can produce a dated move-out video showing intact carpet. Most tenants don't think to document at move-in, when no dispute is even on the horizon, and then wish they had when the deposit fight arrives a year or two later. If you're reading this at the start of a tenancy, the single best thing you can do for your future deposit is take those move-in photos today. And if you're already past move-in, move-out documentation alone is still strong, so plan to capture it thoroughly when the time comes.

If the landlord still refuses, or fails to provide the required itemized statement, you can sue in small claims court — in New York City, for amounts up to $10,000 — to recover your deposit and possibly the interest owed on it. Small claims court is designed for ordinary people to bring exactly these kinds of cases without a lawyer, for a modest filing fee, presenting their own documents. This is the workhorse remedy for deposit disputes, and it's far more accessible than the word "sue" makes it sound. In court, you can rely on Article 7 of the General Obligations Law, which is the body of New York law that governs rent security deposits, and you present your evidence — the checks and receipts showing you paid your rent, the photos showing the unit's condition, the repair invoices or their absence — to establish that you met your obligations and left the place in good shape. The law is on the books, your evidence is in your folder, and small claims court is where the two meet to get your money back.

It's worth dissolving the intimidation that the word "court" carries, because that intimidation is often what stops tenants from recovering money that's plainly theirs. Small claims court was built precisely so that people without lawyers, without legal training, could resolve disputes like this one. You file a simple form, pay a small fee, and on your court date you tell your side and hand the judge your documents — the lease, the dated photos, the proof you paid rent and moved out on time, and the evidence that the landlord either kept your deposit without the required itemized statement or charged you for normal wear and tear. Deposit cases are among the most common and most straightforward matters small claims courts handle, and the legal framework is squarely on your side: a capped deposit, a strict deadline, a narrow list of lawful deductions, and a forfeiture rule for landlords who don't itemize. You're not walking in to argue some novel or uncertain point of law. You're walking in to show that the landlord broke clear, specific rules, with the documents to prove it. Many landlords, knowing this, settle once a tenant actually files — because they understand their position is weak and the rules favor the tenant. The filing itself is often what breaks the logjam.

There's also a less adversarial route worth knowing about: the New York Attorney General's Office offers mediation services to help tenants recover wrongfully withheld deposits and interest. Mediation can be a faster, less confrontational path than court — a process where a neutral party helps you and the landlord reach a resolution — and it can be especially useful if you'd prefer to avoid the formality of a lawsuit or want to try resolving things more quickly. It's one more avenue in your toolkit, and for some disputes it's the most efficient one. Between a written demand, mediation through the Attorney General's office, and small claims court, you have a graduated set of options, and you can escalate as far as you need to until your deposit comes back.

Step back and look at the full shape of what New York guarantees you, because it's a remarkably tenant-protective framework once you see it whole. The amount is capped at one month's rent, with no stacking of "last month's" on top. In larger buildings, the money must be held in trust, in a disclosed bank account, earning interest that belongs to you. Deductions are limited to a short list of legitimate categories, normal wear and tear can't be charged to you, and every withheld dollar must be itemized in writing — on pain of the landlord forfeiting the right to keep anything if they don't. You can demand a pre-move-out inspection to head off surprise deductions, and the balance must be back in your hands within 14 days. And if any of that is violated, you have remedies that run from a written demand through Attorney General mediation to small claims court, backed by Article 7 of the General Obligations Law.

Here's the reframe to carry out of all this. A security deposit can feel like money you've surrendered — handed over and out of your control, to be returned or not at the landlord's discretion. But that's not what it is, and it's not what the law says it is. The deposit remains your money throughout, held under rules so specific that a landlord who mishandles it leaves clear, provable violations in their wake. The capped amount, the trust account, the itemization requirement, the 14-day deadline — each of these is both a protection and a tripwire, a rule the landlord must follow and a violation you can point to and enforce if they don't. You're not at the mercy of the landlord's goodwill. You're holding a set of legal guarantees with real teeth.

So know the rules, and use them. Check that you weren't charged more than one month at move-in. In a larger building, expect a disclosed bank and your interest. Request your pre-move-out inspection and fix what's on the list. Hold the landlord to the 14-day return and the written itemization. And if they break the rules, gather your lease and photos and receipts, make your written demand, and escalate to Attorney General mediation or small claims court as needed. The deposit was always yours. New York law gives you the tools to make sure it comes home. Find out what you're owed.