In the world of high-net-worth wealth management, there is a silent predator: financial entropy. To understand its impact, consider the diverging paths of two brothers, each starting with $5 million in capital. Their objectives are identical—preserve the estate, maintain a high-end lifestyle, and pass a legacy to their children. Yet, their results after a decade look like two entirely different asset classes.

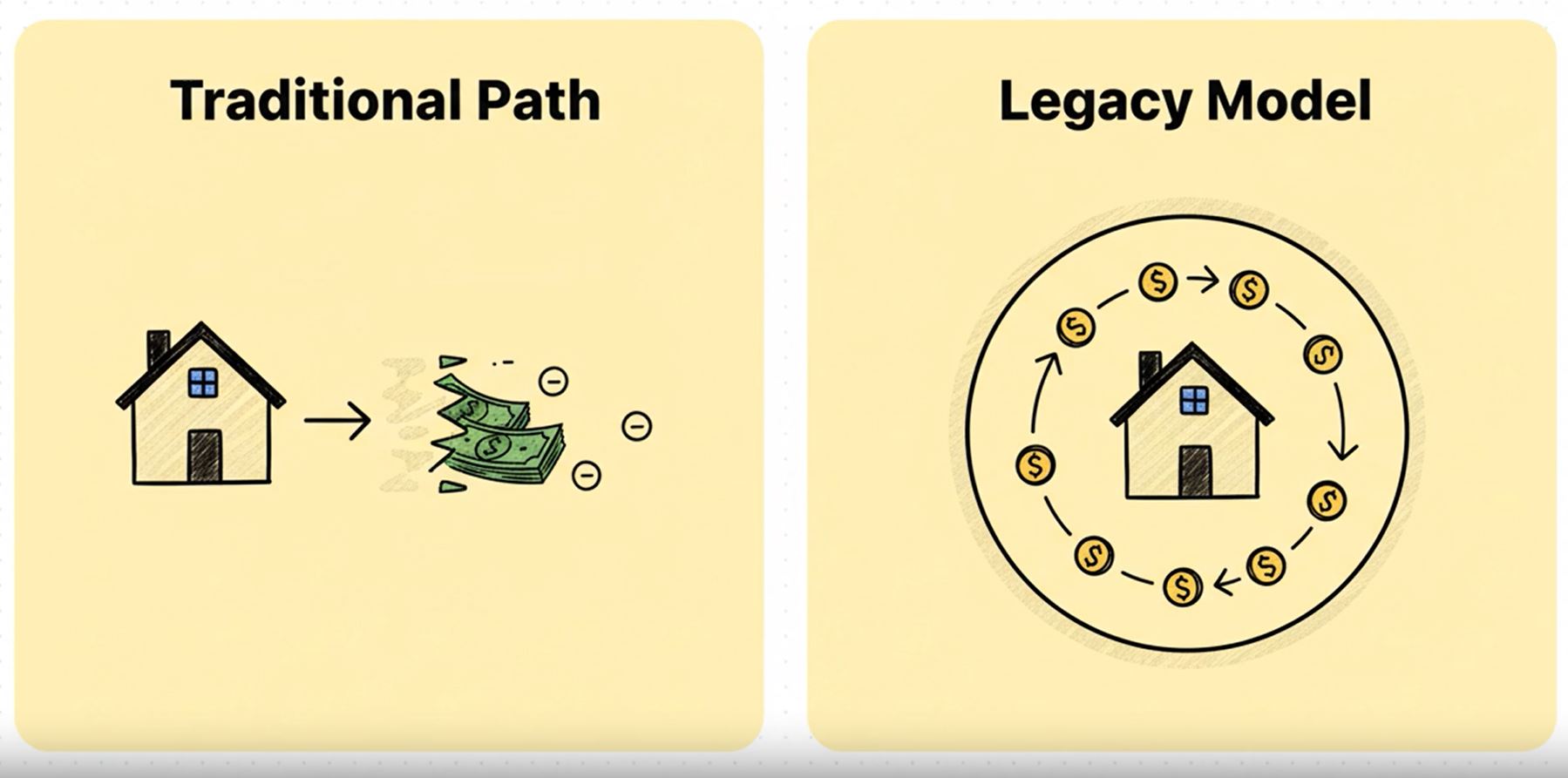

Brother B follows the conventional wisdom of the modern retirement industry. He invests in public markets, withdrawing funds annually to cover his lifestyle and the resulting tax obligations. This "sell assets, pay taxes, repeat" cycle triggers a mathematical certainty of wealth attrition. By the time his estate reaches his heirs, they will receive the mere scraps of a once-great fortune, diluted by repeated tax events at every title change.

Brother A, however, approaches his wealth as a Strategy Architect. He utilizes a Real Estate Limited Partnership (RELP) structure, colloquially known as the "Legacy Game." Instead of allowing his capital to leak through the cracks of the tax code, he builds an engineered system designed for compounding, tax efficiency, and the delivery of undiluted wealth.

The fundamental difference between these two paths begins with the efficiency of their capital. In the RELP structure, Brother A understands that timing is the most potent lever in his portfolio.

“Gaining a dollar today is always better than tomorrow, and paying a dollar today is worse than paying it later.”

By leveraging 100% bonus depreciation in Year 1, Brother A captures an immediate $1.85 million in tax savings. This is not a mere deferral; it is an architectural "head start." This $1.85 million remains within the family office, compounding immediately, whereas Brother B suffers from chronic "structural leakage"—annual tax hits that drain his principal before it can grow. Over a 10-year outlook, this upfront capital advantage creates a wealth gap that traditional portfolios can never bridge.

Most high-net-worth individuals view luxury as a net-cost activity that depletes their estate. For Brother B, a $100,000 vacation effectively costs $150,000 in gross earnings once capital gains taxes and withdrawal penalties are factored in. He is essentially burning his principal to fund his memories.

In contrast, the RELP structure allows Brother A to integrate his lifestyle into his business strategy. By utilizing the partnership’s ranch assets and global barter arrangements, five weeks of luxury lifestyle are treated as a legitimate, pre-tax family business expense. This synthesis of lifestyle and tax efficiency ensures that "vacationing" becomes a preservation of principal. Brother A enjoys the same high-end utility as his brother, but he does so using pre-tax dollars, leaving his core capital untouched.

The traditional "sell assets, pay taxes, repeat" model is a trap of perpetual liquidation. To generate cash flow, Brother B must trigger a taxable event every year. This creates a friction-heavy environment where the government is a silent partner in every transaction.

Brother A escapes this cycle through K-1 distributions. The RELP provides a stream of perpetual passive income that flows to heirs with significantly lower effective taxation and zero requirement for forced liquidation. Because the assets are held within the partnership structure, the estate avoids the tax-heavy title changes and "death taxes" that typically dismantle family wealth. The result is the delivery of undiluted wealth—an intact, income-generating machine passed from one generation to the next.

Public markets are defined by price swings and external shocks—interest rate hikes, geopolitical shifts, and the constant threat of forced selling during a downturn. Brother B’s wealth is a hostage to market sentiment.

The RELP offers a superior risk profile by focusing on the ownership of debt-free real estate. This strategy utilizes "vertical integration"—bringing maintenance, leasing, and management in-house—to fix operating expenses. Consequently, when inflation rises, rental income increases while expenses remain stable, creating a powerful inflation hedge. Most importantly, the value of the RELP is tied to the strength of its rental contracts and ongoing cash flow, not fluctuating property sale prices.

“The RELP structure lets you capture tax benefits today, enjoy superior lifestyle today, and deliver undiluted wealth to future generations — all while avoiding the repeated tax hits that erode traditional retirement accounts.”

The most common critique of the RELP is its reduced liquidity. Transferring interests in a private partnership is not instantaneous; it requires General Partner approval and time. However, to a Wealth Strategy Architect, this is not a downside—it is a strategic constraint.

Liquidity is often the enemy of legacy. It enables the impulsive liquidation and "forced selling" that ruins traditional estates during market panics. When a structure already provides reliable, tax-efficient passive income and a luxury lifestyle, the need for liquidity evaporates. This "illiquidity" serves as a protective barrier, ensuring the family’s core assets remain un-leveraged and intact for decades to come.

The divergence between Brother A and Brother B is a matter of design. One has built a retirement account—a declining pool of capital intended to be spent down until it is gone. The other has engineered a multi-generational legacy—a self-sustaining system designed to grow, protect, and provide.

Traditional wealth strategies prioritize the convenience of liquidity at the steep cost of capital efficiency. The "Legacy Game," through the RELP structure, prioritizes the preservation of principal and the minimization of structural leakage. As you review your own estate, you must ask: Is your strategy designed to fund your retirement, or is it engineered to preserve the undiluted wealth of your future generations?